Blog Posts

Reducing Insurance Premiums with Certified Hot Work Habitats in 2026

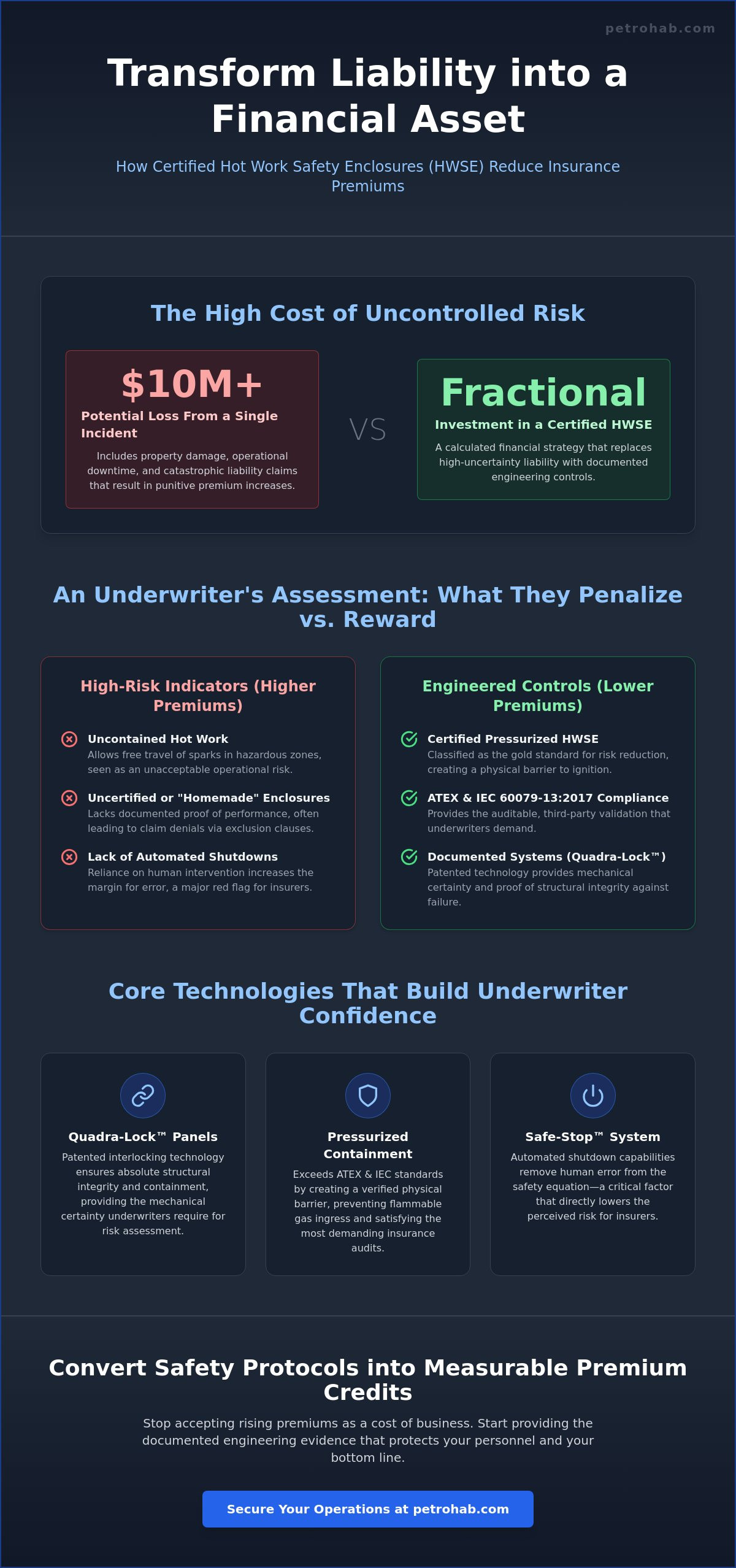

Could a single engineering decision transform your insurance policy from a massive operational liability into a documented financial asset? Asset managers and safety engineers understand that rising premiums for high-risk offshore and onshore activities are becoming unsustainable. You’re likely struggling to prove rigorous risk mitigation to underwriters who see hot work as a catastrophic liability. This article demonstrates how reducing insurance premiums with certified habitats is a tangible reality for operators who prioritize technical compliance and operational excellence.

We’ll examine how deploying PetroHab Hot Work Safety Enclosures (HWSE) equipped with Quadra-Lock panels and Safe-Stop systems provides the precise data underwriters require to lower General Liability and Pollution Insurance costs. By integrating pressurized habitats that meet IEC 60079-13:2017 and ATEX standards, your facility can achieve zero-incident operations while satisfying the most demanding insurance audits. It’s time to move beyond basic fire prevention and adopt a solution that protects both your personnel and your bottom line. We will detail the specific engineering benchmarks that convert safety protocols into measurable premium credits.

Key Takeaways

- Analyze the ‘Risk vs. Premium’ ratio to understand why underwriters penalize uncontained hot work and how engineered containment mitigates these financial liabilities.

- Identify the specific pathways for reducing insurance premiums with certified habitats by aligning operational protocols with ATEX and IEC 60079-13:2017 standards.

- Recognize why pressurized HWSE systems are classified as the gold standard for risk reduction, directly influencing General Liability and Pollution Insurance assessments.

- Establish a professional framework for communicating technical safety data and certification credentials to insurance brokers and underwriters.

- Evaluate how the integration of Quadra-Lock panels and Safe-Stop systems provides the documented evidence necessary to satisfy rigorous 2026 insurance audits.

The Financial Impact of Hot Work Risks in 2026

Hot work remains the leading cause of property loss and industrial insurance claims across the energy and manufacturing sectors. In 2026, underwriters no longer view uncontained welding, grinding, or cutting as an acceptable operational risk. They apply a strict ‘Risk vs. Premium’ ratio where the absence of engineered controls results in punitive rate increases or the total withdrawal of coverage. For a comprehensive technical foundation, consulting a Hot Work Safety Overview helps define the high-stakes hazards involved in these daily activities. When sparks are allowed to travel freely in a hazardous environment, the financial liability doesn’t just rest on the immediate damage; it extends to months of facility downtime and lost production revenue.

The financial disparity between proactive prevention and reactive catastrophe is massive. While implementing a certified PetroHab Hot Work Safety Enclosure (HWSE) involves a clear procurement cost, it’s a fraction of the potential $10 million loss associated with a single ignition incident. Reducing insurance premiums with certified habitats is a calculated financial strategy that replaces high-uncertainty liability with documented engineering controls. True certification means more than just using fire-resistant fabrics. It signifies a proven ignition prevention system that integrates pressurized containment with automated shutdown capabilities like the Safe-Stop Automatic Shutdown System.

To better understand the broader context of insurance premium management, watch this helpful video:

High-Stakes Hazards: Why Underwriters Care

In Zone 1 and Zone 2 environments, the presence of flammable gases and vapors makes uncontained hot work a critical threat. Underwriters recognize that a single stray spark can trigger a catastrophic General Liability claim that impacts the entire corporate balance sheet. They prioritize engineered solutions because these systems remove human error from the safety equation. Industrial hot work risk is the primary variable in premium calculation for energy firms. Consequently, reducing insurance premiums with certified habitats becomes much easier when you can present a technical plan that includes pressurized containment as a baseline requirement.

The Hidden Cost of Uncertified Enclosures

Deploying ‘homemade’ or uncertified habitats is a significant strategic error that often increases liability. These systems frequently utilize materials that aren’t truly fire-rated or lack the structural integrity to maintain positive pressure. Insurance carriers are increasingly inserting ‘exclusion clauses’ that may deny claims if an incident occurs while using non-certified equipment. Unlike the precision-engineered Quadra-Lock panels used in PetroHab systems, uncertified enclosures offer no legal or technical protection during an audit. Using unverified equipment tells an underwriter that your facility doesn’t value rigorous compliance, leading to higher rates and stricter policy terms.

How Insurance Underwriters Evaluate Industrial Risk

Underwriters in the heavy industry sector don’t rely on generic risk profiles. They perform granular assessments of facility-specific hazards. By demonstrating a commitment to reducing insurance premiums with certified habitats, operators provide tangible evidence of risk containment. The underwriting process meticulously converts these safety protocols into specific premium figures. Insurers prioritize engineered controls because they offer a physical barrier between ignition sources and hazardous atmospheres.

A critical component of this evaluation is structural integrity. Patented Quadra-Lock technology ensures that panels remain securely interlocked even under significant pressure. This mechanical certainty is what underwriters look for when assessing the potential for containment failure. Compliance with OSHA hot work precautions regarding physical isolation is no longer just a regulatory requirement; it’s a financial necessity. When a system provides documented proof of containment, it shifts the risk profile from high-uncertainty to a controlled operational variable.

Engineered Controls vs. Administrative Controls

Insurers distinguish sharply between administrative controls, such as manual fire watches, and engineered controls like a PetroHab Hot Work Safety Enclosure (HWSE). While administrative measures rely on human vigilance, engineered systems provide constant, fail-safe protection. Underwriters view the reliability of automatic gas detection and the Safe-Stop Automatic Shutdown System as superior to manual monitoring. For a deeper technical analysis, operators should review A Comprehensive Guide to Advanced Hot Work Safety Systems in 2026.

Reducing Business Interruption (BI) Exposure

Business Interruption (BI) insurance often constitutes a significant portion of total coverage costs. Certified habitats allow for hot work on live platforms without requiring a full facility shutdown. From an underwriter’s perspective, the ability to isolate hazardous activities means there’s a much lower probability of a facility-wide outage. Reducing insurance premiums with certified habitats is achieved by lowering the BI exposure during essential maintenance cycles. Maintaining production levels while performing critical repairs creates a dual benefit of operational efficiency and reduced risk profile. To ensure your facility meets these rigorous underwriting standards, you can evaluate our certified pressurized habitats for your next project.

The Link Between Certification and Premium Reductions

Insurance underwriters don’t grant credits based on verbal assurances. They require documented technical validation. Reducing insurance premiums with certified habitats is directly tied to the presence of third-party verified safety markers such as ATEX, IECEx, and NFPA 51B. These certifications provide a data-backed guarantee that a system will perform as engineered during a hazardous event. While many enclosures claim fire resistance, underwriters distinguish between a simple spark-containment tarp and a precision-engineered PetroHab Hot Work Safety Enclosure (HWSE). Fire resistance is a reactive property, but true ignition prevention is a proactive engineering control that insurers reward with lower rates.

Positive pressure certification is a critical benchmark in this evaluation. It proves through rigorous testing that the internal atmosphere of the habitat remains at a higher pressure than the external environment. This pressure differential ensures that flammable gases cannot enter the work area, effectively neutralizing the risk of explosion. When an operator deploys a system with this specific certification, they provide insurers with a physical certainty that manual fire watches cannot match. Furthermore, the integration of the Safe-Stop Automatic Shutdown System elevates a facility to ‘best-in-class’ status. This system automatically terminates hot work if pressure is lost or gas is detected, satisfying the most stringent risk mitigation requirements of 2026.

ATEX and IECEx: The Global Benchmarks

Global standards like ATEX and IECEx provide a universal language for risk managers and insurers to assess equipment reliability. For offshore assets, Zone 1 and Zone 2 compliance is non-negotiable. These certifications confirm that every component, from the Quadra-Lock panels to the ventilation units, is safe for use in potentially explosive atmospheres. To understand how these requirements impact your operational strategy, refer to Hazardous Environment Standards: The 2026 Guide to Global Compliance and Hot Work Safety. Using hardware that lacks these global stamps of approval often results in significant premium surcharges or coverage denials.

NFPA 51B and OSHA Compliance

Meeting the minimum regulatory requirements is the first step toward stabilizing insurance costs. NFPA 51B compliance is often a prerequisite for industrial fire insurance coverage. However, simply meeting the code isn’t enough to secure the best possible rates. By going ‘above-code’ with a fully pressurized HWSE, companies demonstrate a superior commitment to loss prevention. This proactive stance allows brokers to negotiate discretionary premium credits that aren’t available to firms only meeting the bare minimum. Reducing insurance premiums with certified habitats becomes a straightforward process when you can present underwriters with a safety plan that exceeds standard OSHA requirements through advanced engineered containment.

Best Practices for Presenting HWSE Usage to Insurers

Procurement and safety teams must collaborate to translate technical safety features into tangible financial benefits. Underwriters require concrete proof of risk mitigation rather than vague promises of safety. Reducing insurance premiums with certified habitats depends on your ability to provide a comprehensive technical data package. This package serves as the definitive evidence of your facility’s commitment to ignition prevention. It moves the conversation from abstract safety goals to measurable engineering benchmarks.

The creation of a Risk Mitigation Dossier is the most effective way to influence an underwriter’s decision. This document should move beyond basic safety manuals and focus on technical specifications. Technical data sheets act as linguistic anchors for quality and compliance in the eyes of an insurer. By providing these documents upfront, you demonstrate a level of meticulousness that instills absolute confidence in your risk management strategy.

The Risk Mitigation Dossier

- Step 1: Attach full ATEX and IECEx certification documents for the specific PetroHab Hot Work Safety Enclosure (HWSE) units in use. This provides the third-party validation insurers require for high-risk Zone 1 and Zone 2 environments.

- Step 2: Document the integration of the Safe-Stop Automatic Shutdown System. Explain how this technology provides an automated, fail-safe response to gas detection or pressure loss, effectively removing human error from the ignition prevention equation.

- Step 3: Highlight the structural reliability of Quadra-Lock panels. Emphasize their performance in high-wind or offshore environments where standard containment systems often fail to maintain positive pressure.

Collaborating with Your Insurance Broker

Effective communication with your insurance broker is vital for securing favorable terms. You should explicitly ask for a discretionary credit based on your use of engineered safety controls. Many brokers are unaware of the specific technical advancements in pressurized habitats, so education is necessary. Inviting underwriters to witness a pressurized habitat setup in person can build significant confidence in your operations. When they see the Quadra-Lock panels in a live configuration, the abstract concept of safety becomes a visible, measurable engineering reality. Using third-party training and supervision certificates serves as additional proof of personnel competency.

Reducing insurance premiums with certified habitats is a long-term strategic objective. While the hardware provides immediate protection, your zero-incident history provides the necessary proof of efficacy over time. By documenting every instance where an HWSE prevented a potential hazard, you build a case for lower General Liability and Pollution Insurance rates. This proactive approach transforms safety from a cost center into a strategic financial advantage. To begin building your technical risk dossier, consult our engineering team for full HWSE specifications.

PetroHab HWSE: Engineering Financial and Operational Security

PetroHab is the global benchmark in certified hot work containment. In high-hazard environments, safety managers require equipment that performs without compromise. Our systems provide a dual benefit. They protect personnel while simultaneously protecting the corporate bottom line from catastrophic liability. Reducing insurance premiums with certified habitats isn’t a passive outcome; it’s the result of deploying rigorous engineering. By choosing an industry leader, facility managers signal to underwriters that they’ve replaced high-risk variables with controlled, technical solutions. This proactive stance is essential for maintaining operational continuity in the demanding landscape of 2026.

Operational security depends on the reliability of ignition prevention systems. When a facility deploys a PetroHab Hot Work Safety Enclosure (HWSE), it implements a barrier that’s been tested against the most stringent international standards. This commitment to technical excellence reduces the probability of a multi-million dollar ignition event. It transforms safety from a regulatory burden into a strategic financial asset. Insurers recognize this distinction and reward the use of verified technology with more favorable policy terms and lower deductibles.

Unmatched Structural Integrity with Quadra-Lock

The Quadra-Lock system defines habitat integrity. Unlike standard panels that may buckle or leak under pressure, these modular interlocking components create a secure, airtight seal. This structural certainty is vital for offshore assets facing high-wind loads or extreme weather conditions. For a detailed technical breakdown of these systems, consult Pressurized Welding Habitats: The Definitive Guide to HWSE Technology. Choosing an interlocking system provides the financial peace of mind that underwriters value during risk assessments. It ensures that positive pressure is maintained at all times, which is the core requirement for reducing insurance premiums with certified habitats.

Safe-Stop: The Ultimate Risk Mitigation Tool

The Safe-Stop Automatic Shutdown System acts as an internal insurance policy. It continuously monitors for gas ingress and pressure loss within the habitat. If a hazard is detected, the system immediately terminates power to all hot work equipment. This logic-driven response eliminates the delays and errors inherent in manual fire watches. Dual-gas sensing and automatic pressure monitoring provide the high-fidelity data required to satisfy 2026 insurance audits. When the hardware itself manages the risk, the facility’s overall liability profile drops significantly. Safety managers must move beyond legacy containment methods and embrace automated protection to ensure future compliance. Contact PetroHab today to secure your 2026 hot work safety fleet and optimize your facility’s risk profile through engineered excellence.

Securing Operational Continuity and Financial Resilience

Industrial asset protection in 2026 requires a precise alignment between safety engineering and financial risk management. This article has detailed how underwriters prioritize engineered controls over simple administrative fire watches. By utilizing systems that feature ATEX and IECEx certified components, operators provide the technical validation required to move beyond standard compliance. Implementing these protocols remains the most direct path toward reducing insurance premiums with certified habitats while maintaining production on live platforms.

PetroHab’s patented Quadra-Lock technology ensures structural integrity in the most demanding environments. Our systems are backed by a global track record in offshore and onshore safety, offering a definitive technological remedy for ignition hazards. Transitioning to a certified fleet doesn’t just protect your personnel; it converts your safety program into a measurable financial asset. You can take the first step toward optimizing your facility’s risk profile today. Request a quote for certified PetroHab HWSE units to lower your operational risk and ensure your operations remain resilient against both physical hazards and rising insurance costs.

Frequently Asked Questions

Does using a welding habitat really lower insurance premiums?

Yes, insurers often grant discretionary credits when operators deploy engineered controls that demonstrably lower the probability of ignition. Reducing insurance premiums with certified habitats is possible because these systems provide the technical validation underwriters require to move a project from a high-risk to a controlled-risk category. This shift directly influences the calculation of General Liability and Business Interruption figures by providing a documented layer of protection.

What specific certifications should I look for to satisfy my insurer?

You must prioritize ATEX and IECEx for hardware safety and NFPA 51B for procedural compliance. These international standards provide a universal language for risk managers and underwriters to assess equipment reliability. Insurers look for these specific certifications to confirm that the habitat can maintain positive pressure and effectively isolate ignition sources in Zone 1 and Zone 2 environments. Without these markers, the equipment is often viewed as a liability rather than a safety asset.

Can I use an uncertified habitat and still get an insurance discount?

No, using uncertified equipment typically increases your liability rather than reducing it. Insurers may view uncertified habitats as a sign of negligence, which can lead to higher premiums or the activation of exclusion clauses in your policy. To achieve the goal of reducing insurance premiums with certified habitats, the equipment must have third-party validation from recognized bodies. Uncertified systems lack the structural certainty provided by technologies like Quadra-Lock panels.

How do automatic shutdown systems like Safe-Stop affect my risk profile?

Automatic shutdown systems like Safe-Stop significantly improve your risk profile by removing human error from the safety equation. These systems provide a fail-safe response to gas detection or pressure loss, which underwriters view as a superior risk mitigation measure. This technological redundancy often satisfies best-in-class requirements for large-scale energy projects. It replaces manual monitoring with a precise, engineering-driven solution that ensures immediate cessation of hot work during a hazard.

What is the ROI of leasing vs. buying a certified HWSE for insurance purposes?

The ROI for insurance purposes is identical whether you lease or buy, as long as the hardware maintains its certification. Leasing allows for lower upfront costs on short-term projects while still providing the necessary documentation to satisfy brokers. Buying is a strategic long-term investment that builds a permanent zero-incident history, which is essential for negotiating future rate reductions. Both options provide the same level of engineered risk containment for your facility.

Will my insurer require proof of technician training for the habitat?

Insurers frequently request training certificates to verify that personnel can properly deploy and monitor the pressurized habitat. Hardware alone isn’t sufficient; the competency of the technicians ensures that the engineered controls are utilized correctly. Documented training programs act as additional proof of a rigorous safety culture during an insurance audit. Providing these records alongside technical data sheets reinforces the reliability of your entire hot work program.

How does NFPA 51B compliance relate to my insurance coverage?

NFPA 51B compliance is a fundamental requirement for most industrial fire insurance policies. While simple compliance avoids surcharges, using a PetroHab HWSE goes above-code by providing pressurized containment. This proactive approach allows your broker to argue for credits that aren’t available to facilities only meeting the bare minimum regulatory standards. It demonstrates a commitment to exceeding industry benchmarks for fire prevention and personnel safety.

What happens to my insurance if a hot work incident occurs inside a certified habitat?

If an incident occurs, having a certified habitat provides documented proof of due diligence and risk mitigation. This evidence protects the operator from claims of gross negligence and helps ensure that the insurance claim is processed according to the policy terms. The use of Quadra-Lock panels and Safe-Stop systems demonstrates that every reasonable engineering step was taken to prevent the event. It provides a legal and technical shield during the post-incident investigation.